Investing Is “Risky” Business – Conclusion - Part 5 of 5

By Mike Fortunato, CIM®, FCSI®

image:FHM.com - Warner Bros.

This is the fifth and final instalment in our five-part series about risk. In the previous instalments we introduced three types of risk that investors need to consider when trying to achieve an investment goal: Volatility Risk, Shortfall Risk and Absolute Risk. We then took a deeper look at each type of risk and discussed ways to manage them. In this last instalment I want to illuminate the relationship among these three risks and suggest some strategies that exploit these connections to lower overall risk and help us reach our goals.

Let’s quickly summarize each risk, and my recap my tips for managing them:

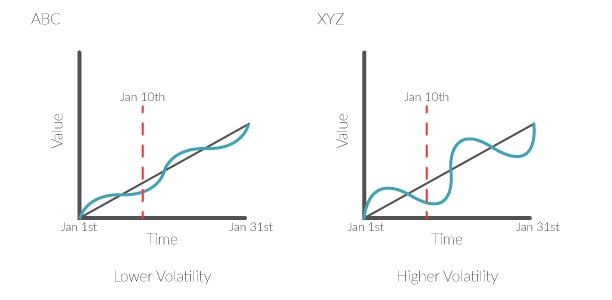

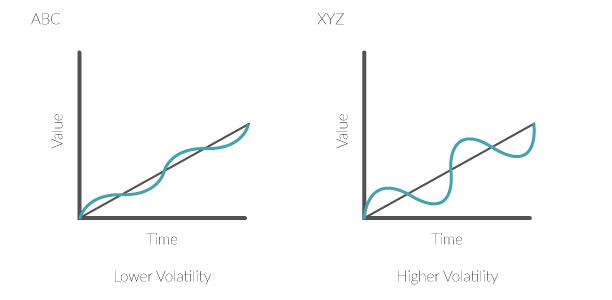

Volatility Risk refers to the potential fluctuations in value an investment may experience while owned. It doesn’t represent a realized loss (or gain) unless that investment is sold. Generally speaking, the investments that have historically provided the highest potential return also tend to have higher volatility, whereas the investments with the lowest volatility have tended to have the lowest return. I believe that Volatility Risk is best managed by ensuring your portfolio’s volatility is appropriate for your time horizon. Investors with longer time horizons are in a better position to accept more Volatility Risk, because there is adequate time for their portfolio to recover from a “paper-loss”. Conversely, if an investor has a shorter time horizon, then they should opt to hold investments that are less volatile. By properly constructing a portfolio that complements their time horizon, investors create a situation where they are insulated from the negative effects of volatility. The benefit of managing Volatility Risk with an appropriate time horizon is that investors don’t have to limit security selection to low volatility choices investments that come with lower return; investors, however, do need to be mindful that unplanned emergency withdrawals will reintroduce the effects of Volatility Risk back into the equation.

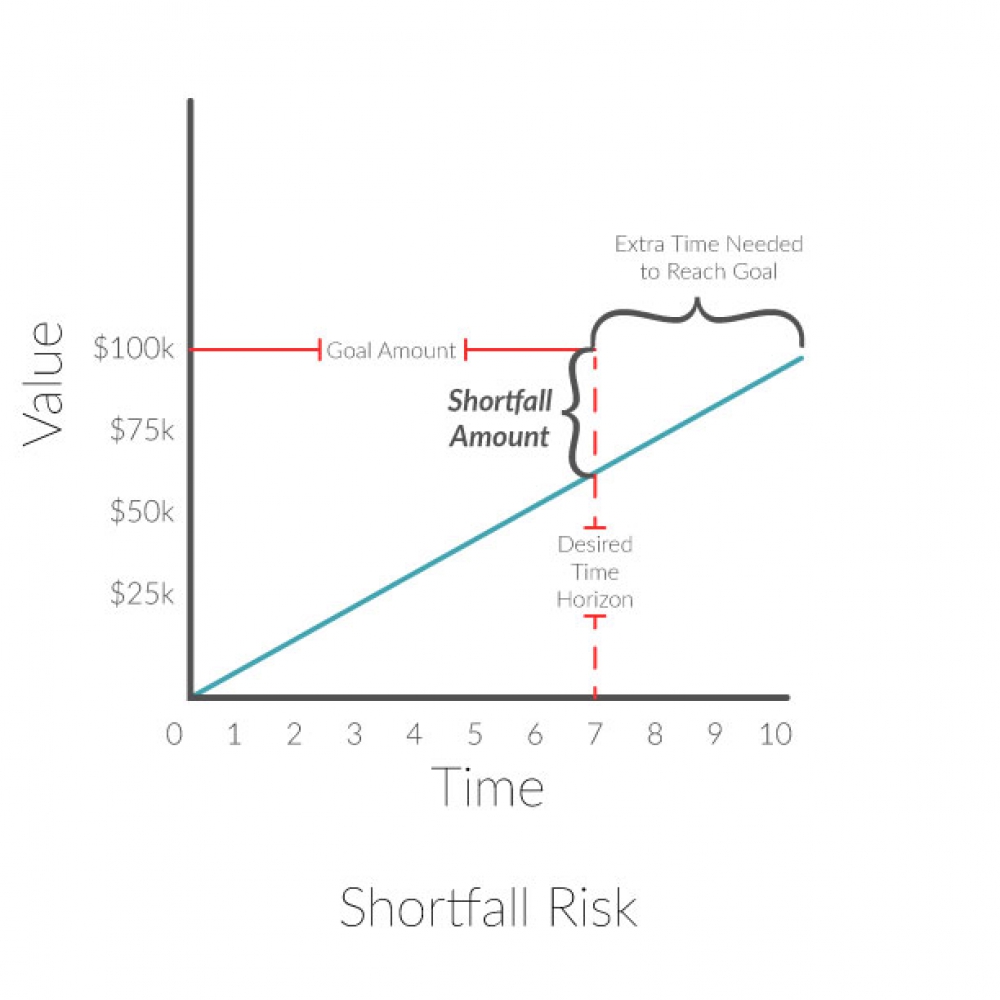

Shortfall Risk is the potential of not reaching an investment goal because the actual rate of return received was less than the expected rate of return. Beyond achieving a satisfactory rate of return, which goes without saying, there are two things investors should focus on that will help minimize shortfall risk:

- Striving to contribute more money towards the goal, as frequently as possible.

- Making sure their goal is realistic given their time horizon and situational constraints.

Like Volatility Risk, the best ways to combat Shortfall Risk come from behaviours that go beyond security selection and instead focus on the larger picture of the investors goal and plan to achieve it.

Absolute Risk is the risk of experiencing some sort of personal catastrophe or emergency. It is unlike the above two risks because it is only indirectly related to the investor’s goal; however, it has the ability to derail an investment plan because it may force an investor to stop saving, or worse, withdraw from their plan. The best way to combat this risk is to put yourself in a situation where it won’t affect your investment plan. This can be accomplished by insulating your investments from a personal emergency by having both an emergency fund and adequate insurance.

As you can see these three risks are huge obstacles that investors must navigate if they are going to reach their goals. Although these risks impact different aspects of an investor’s plan, they are connected in ways which can be exploited. One common thread these risks all share is that they can all largely be managed through how an investment plan is structured in relation to the goal it is trying to achieve.

Prioritizing these three risks is the key to combating them. Even though Shortfall Risk is the most important of the three risks I tend to make it my last priority because it can be largely solved by first controlling the other two risks. As we saw above, beyond achieving a satisfactory rate of return, two habits that minimize Shortfall Risk are:

- Striving to contribute more money towards the goal, as frequently as possible.

- Making sure the goal is realistic given the time horizon and situational constraints.

Both of these items are staples of a solid financial plan; however, the first habit can be disrupted if an Absolute Risk materializes. More specifically, investors might be compelled to tap their investments for funds in the event of a personal emergency. Viewed in this way, Absolute Risks are actually a potential cause of Shortfall Risks. By having an emergency fund and adequate insurance investors not only mitigate the effects of Absolute Risks, but also help indirectly minimize Shortfall Risks.

The second habit that helps minimize Shortfall Risks is making sure that investors’ goals are realistic given their time horizon and situational constraints. As you may recall, however, the exercise of taking a broad view of an investment plan in the context an end goal is an indispensable tool that investors can use to insulate themselves from Volatility Risks. My view has always been that rather than run from volatility, investors should first see if they can create a financial plan that can embrace volatility and the return that can be correlated with it. The only caveat of this approach is that investors need to ensure that they can adhere to their time horizon and not be compelled to alter their investment plan to cover a temporary life emergency with investment funds. But we already addressed this earlier by first focusing on Absolute Risk, through having an emergency fund and insurance.

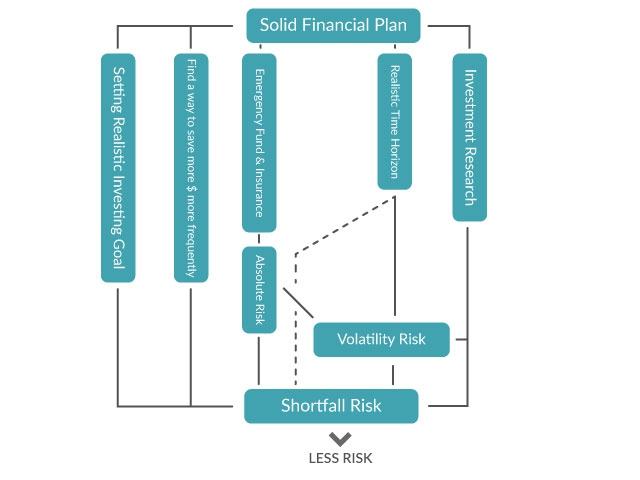

Below I’ve created a flow-chart to help illustrate how I mentally prioritize these risks. This chart isn’t the only solution to the problem of managing these risks, it just happens to be a structure that has worked well for the financial plans I’ve help create. Starting at the top the chart flows towards the risk that represents ultimate failure: Shortfall Risk. However, you will notice that Shortfall Risk is the last step in the flow-chart because it is largely combated by first solving the other elements in the chart.

In conclusion, I believe that Volatility Risk, Shortfall Risk & Absolute Risk are the three most important risks that stand in the way of investors reaching their goals. Individually these risks have the potential to hurt an investment plan, but also, when mismanaged, their negative effects can be compounded. By prioritizing these three risks investors can leverage how these risks are interconnected and focus on only a few crucial habits to combat their negative effects. Instead of juggling three risks investors can instead view this as a single exercise in creating a solid financial plan that complements their financial goal. These risks will still exist; however, a solid plan will help investors steer clear of those risks while constantly keeping them in view.