4 Investing Lessons from Investing Greats

It’s often said imitation is the sincerest form of flattery. If you’re looking to be the next successful investor, looking to those who have already achieved investment success is a good place to start. Here are four successful investors who provide timeless lessons to learn from that will help shape your investment philosophy. To round out the field we have two Americans and two Canadians.

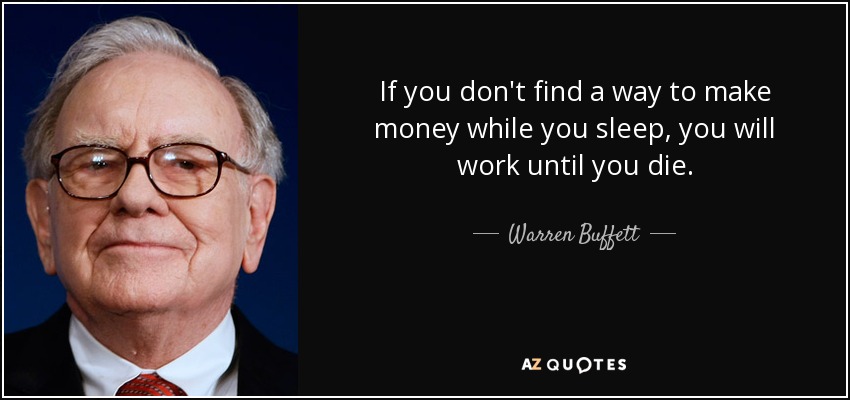

Warren Buffett

Warren Buffet is the Chairman and CEO of Berkshire Hathaway. He’s also arguably the most successful investor the world has ever seen. There’s a never-ending argument over what’s better: active or passive investing. Buffett has clearly picked a side: index investing. Buffett famously made a million-dollar bet: by investing in a low-fee index fund he could outperform a powerful hedge fund. A decade later and Buffett has proved the naysayers wrong, as he managed to do just that.

Investment fees (or MERs) can take a big bite out of your investment portfolio. If you’re looking to build a solid investment portfolio, low-cost investments like ETFs (that Smart Money offers) are your meal ticket to growing your portfolio long-term.

Peter Lynch

If you don’t understand a business, you probably shouldn’t invest in it. That’s one of the many golden investments lessons from American investor Peter Lynch. In fact, he takes it a step further: never invest in any idea you can’t illustrate with a crayon. Lynch once famously took a class of seventh graders out for dinner, illustrating each stock with a little drawing. If an investment is so complex that you have no idea where your money is going, you’re better off not investing. Maybe if more investors followed this lesson during the late 2000’s we could have avoided the financial crisis since few understood how mortgage-backed securities worked.

Kevin O’Leary

Kevin O’Leary has made a name for himself for not being shy to “say it how it is” as a venture capitalist on Dragon’s Den and Shark Tank. O’Leary (or Mr. Wonderful as he likes to call himself) isn’t afraid to speak his mind if he sees a bad idea. When he’s not on TV, O’Leary is a successful investor. One of O’Leary’s golden rules is that he won’t invest in a stock unless it pays a divided. And this makes sense. Many investors chase after yield, but it’s dividends that can make you rich. If you invested in the stock market since 1926, you would have made more money from dividends than capital gains. Divided-paying stocks encourage a long-term investing philosophy. You “buy and how” and watch the money slowly trickle in – and it adds up over time.

Who opened O’Leary’s eyes to dividend investing? It was his dear, old mother. When she passed away, he was amazed at the investment portfolio she had accumulated using dividends. O’Leary has a strict investment rule: if it doesn’t pay a dividend, he won’t buy it. You don’t have to be that strict of an investor, but it’s something to consider.

Derek Foster

Derek Foster is six-time National Bestselling author. He is also Canada’s youngest retiree, leaving the workforce at the ripe, old age of 34. Foster is a millionaire. Despite spending his 20’s backpacking through Europe, he’s a self-made millionaire. How did he do it? By investing his money in recession-proof stocks. For example, when the economy tanks, do people stop brushing their teeth? Of course not! That’s why Foster invests in blue-chip stocks like Colgate. Colgate has been increasing its dividend steadily for decades. Foster is living proof you don’t have to be an investing genius to strike it rich. In his book, The Idiot Millionaire, he shares his secrets of how anyone can achieve investing success like him by following his simple investing philosophies.