(Un)Realistic Investment Expectations - Part 3 - Misinterpreting Historical Data

- By Mike Fortunato, CIM®, FCSI®

This is the third and final installment dedicated to unrealistic investment expectations. In the last installment, we discussed how misunderstanding financial jargon can be both a cause of an investor’s unrealistic investment expectations, and an obstacle impeding communication between an advisor and their client. Today, I’d like to highlight some common flaws in how many investors use historical information to formulate performance and risk projections, which is another cause of unrealistic investment expectations.

Misinterpreting Historical Data

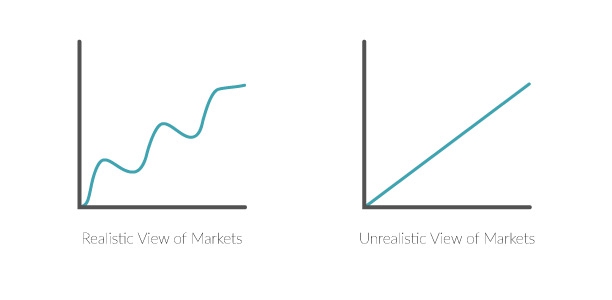

Most investors look to the past for clues when trying to forecast future performance. Although I agree that historical data can teach us a lot about the future, I want to caution investors about some of the more common mistakes that are made when forecasting. It is important to remember that markets and the economy move in cycles. Generally speaking, all cycles have two things in common: a rising-cycle is followed by a falling-cycle, and, a falling-cycle is followed by a rising cycle. This might seem elementary, however, in my experience, most investors ignore this natural fact, and instead assume that the current trend will last forever. I’ve even had many conversations with investors who claim to be aware of fact that markets move in cycles, but then continue basing their long-term projections as if the market moved in a straight line. Many advisors further complicate this misunderstanding by lazily citing market statistics without highlighting the fact that those statistics are actually averages of cyclical data.

The key to avoiding this fallacy is to always analyze full cycles when considering past data, and if possible, consider multiple cycles. The past can give us some great clues as to what the future might hold, but we need to make sure we are looking far enough in the past when gathering our data to formulate our projections. A realistic forecast understands that there will be cycles in the future, as there were in the past. And unrealistic forecast presumes that the current phase of the cycle will last forever. Investors need to remind themselves that every bull market eventually leads to a bear market, and vise versa.

The key to avoiding this fallacy is to always analyze full cycles when considering past data, and if possible, consider multiple cycles. The past can give us some great clues as to what the future might hold, but we need to make sure we are looking far enough in the past when gathering our data to formulate our projections. A realistic forecast understands that there will be cycles in the future, as there were in the past. And unrealistic forecast presumes that the current phase of the cycle will last forever. Investors need to remind themselves that every bull market eventually leads to a bear market, and vise versa.

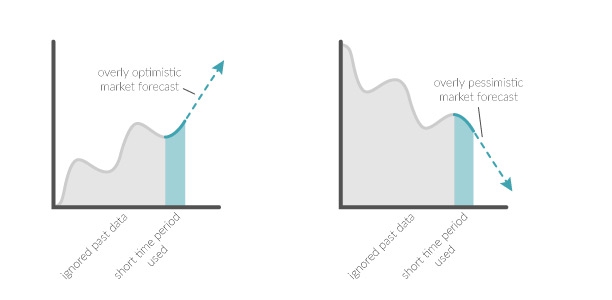

Two related miscalculations many investors also make are:

- Only considering past bull markets when forecasting future return. This will often lead to overly optimistic projections.

- Only considering past bear markets when forecasting future risk. This will often lead to overly pessimistic projections.

It is important to highlight that I don’t think investors are naive; I would actually argue that they are acting quite logically given how long it can take for a trend to reverse. Market cycles can often take years or decades to reveal their full periodicity. In fact, some slower, cyclical economic phenomenon take so long to unfold that text books on the subject are written, published and taught to finance students only to have the phenomenon reverse or change as those students enter the workforce. Investors are also bombarded daily with news and media that tends to focus on the short-term picture and sensationalize outlier events. In light of all these distractions I can totally understand why many investors formulate unrealistic market expectations. Again, this is where great advisors can really make a difference in helping a client focus on the past data they are ignoring.

I hope I’ve been able to illuminate what I believe are two major causes of investor’s unrealistic investment expectations: Financial Jargon & Misinterpreting Historical Data. There are many other potential causes of unrealistic expectations beyond these two; I actually plan on devoting future posts to the discipline of Behavioural Finance, which studies cognitive and emotional biases that cultivate irrational behaviour in investors. Advisors need to remember that although investors often have unrealistic investment expectations, there are perfectly logical reasons why those expectation arise. When advisors take the time to educate their clients, they are usually quick to temper and evolve their forecast. Good advisors know that having a solid investment strategy is worthless if their clients are not willing to stick with it for the long haul. Also, clients are not going to stay invested in strategies that are not compatible with their expectations. That is why great advisors understand that the key to long-term success lies in harmonizing their clients’ expectations with their own. As we already mentioned, investors are typically logical, and usually just lack some foundational wealth management principles. By taking the time to educate their clients, advisors can leverage their clients’ logic and encourage a natural alignment in their views towards having more realistic investment expectations.