Investing Is “Risky” Business – Introduction - Part 1 of 5

By Mike Fortunato, CIM®, FCSI®

image:FHM.com - Warner Bros.

What is risk? What does it mean for something to be risky? Well, the dictionary defines “risk” as: “a situation involving exposure to danger”, and defines “danger” as: ‘the possibility of suffering from harm’. Okay, so risk seems to involve two parts: the element of a negative future consequence, as well as a probabilistic element. But I didn’t need to look up “risk” in the dictionary. After all, everyone intuitively grasps the concept of risk. We all experience risk in our day to day lives. There are physical risks like: driving in a car, walking across the street or riding on a plane or boat, but there are also risks that don’t involve physical harm like: switching careers, starting a new relationship, or gambling. All these examples are considered risky even though the consequences and probabilities are quite different. Clearly, risk can take on many forms. As a portfolio manager and advisor, I’m most concerned with how risk impacts wealth creation and the investments of my clients who have entrusted me with their financial future.

We’ve all heard the phrase: “investing involves risk”, but just like everyday life, risk, as it pertains to wealth management and investing, can take on many different forms. If you ask several people to define “risk”, in the context of investing, you’ll likely receive a diverse set of responses. You’re also bound to hear contrasting opinions as to how to best combat or control those same risks. In this article I plan to illuminate the concept of “risk” and offer some advice on how it can be managed. To tackle this topic, I’ll first need to thoroughly define what I mean by risk, from a wealth management perspective; then I’ll share my observations of how some investors view risk, and finally, I’ll share my own insights and ideas on risk management. It is important to note that there are many varying opinions on how to best manage risk; my views are not necessarily the best, but rather, I’m hoping to offer a different point of view from what is often said about this topic.

There are many different categories and subcategories of risk that affect investors, but for the purpose of this discussion, there are three types that I want to focus on:

- Volatility (sometimes referred to as Variability, Volatility Risk, or sometimes just Risk)

- Shortfall Risk (sometimes referred to as just Shortfall)

- Absolute Risk (sometimes called Pure Risk)

Although these three types of risk are different, they are deeply interconnected to both an investor’s portfolio and financial plan. My goal is to shed some light on those connections and give both investors some new insights to consider.

Volatility:

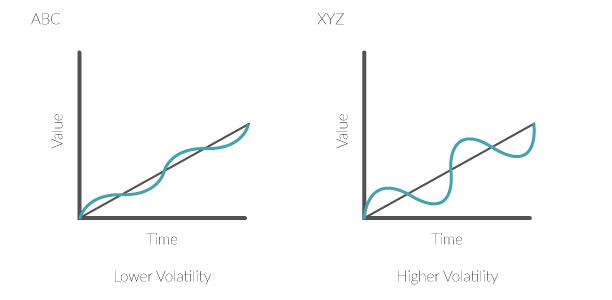

When I say volatility, I’m referring to fluctuation of the price of an asset or value of portfolio as a whole. Volatility is usually measured using “standard deviation”, which measures the dispersion of a data set from its mean or average. Put more simply, volatility refers to the magnitude of the past ups and downs of an asset. For example, in image below we see two different investments: Investment ABC & Investment XYZ. The blue line traces the growth path of those investments over the same time frame. The grey line represents their average growth. As you can see, both Investments have the same average growth: that is, they both start and end at the same value. However, XYZ experienced a bumpier ride, as its ups & downs were twice the size of ABC’s ups & downs. In this scenario, we would say that XYZ was twice as volatile as ABC. We would also say that historically, XYZ carried twice the volatility risk of Investment ABC.

Shortfall Risk:

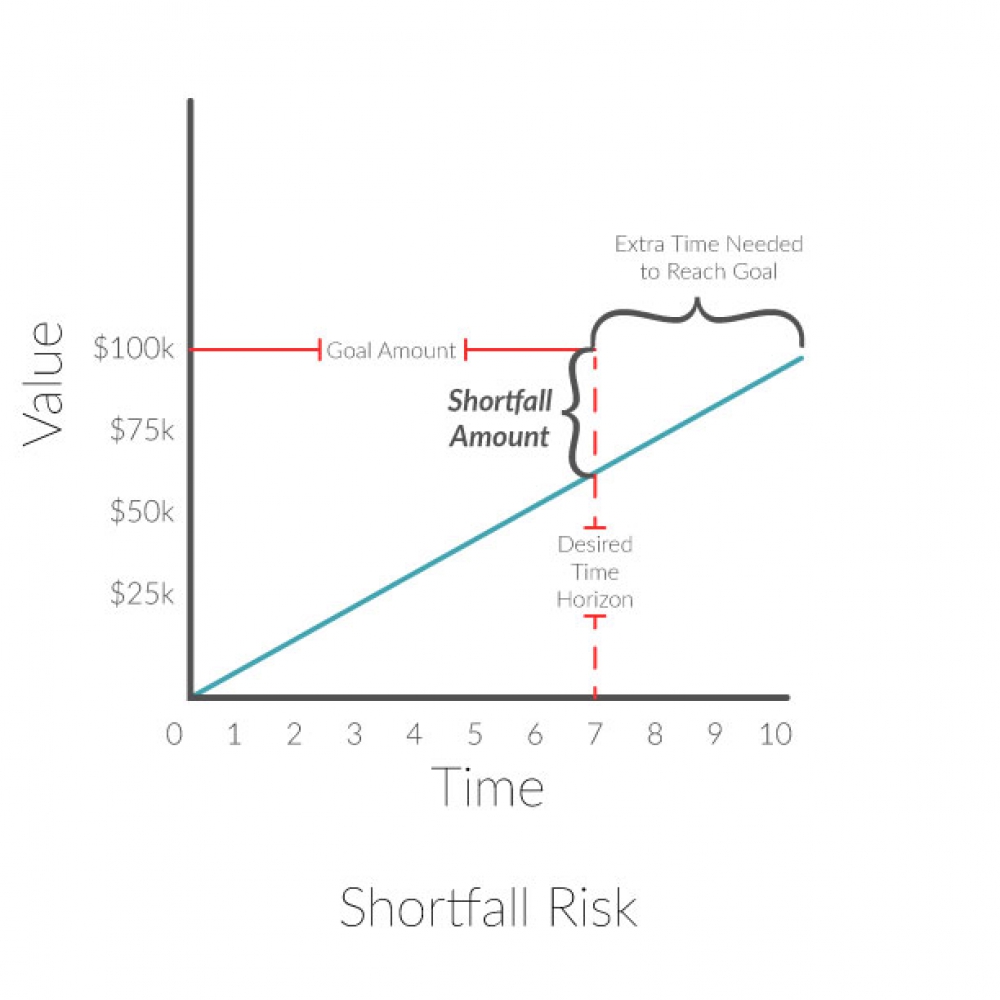

Technically speaking, shortfall risk is the risk that an investment’s actual return will be less than the expected return needed to meet a financial obligation. Another way to think about shortfall risk is to say that it is the risk of falling short of an investment target or goal. For example: the investor below had the goal of reaching $100,000 in seven years. Unfortunately, she was only able to reach $60,000 after seven years of investing. They now had to make choice: settle for only $60,000 or continue to save & invest and extend her time horizon.

Absolute Risk:

When I refer to absolute risk I’m talking about the type of risk that is often associated with insurance. Absolute risk is any risk where there is no possibility of gain; there is only the risk of loss. Examples would include events like: health issues, losing a job, or any sudden, unplanned expense. Absolute risk may not affect an investor’s portfolio directly, but it can damage the overall financial position of the investor, which often impacts their investing behaviours.

Now that I’ve introduced these three related risks, in the next instalment of this article will dig deeper into these three types of risk, and I’ll share some best practices I follow when trying to manage these risks while building wealth for my clients.