Investing Is “Risky” Business – Volatility Risk - Part 2 of 5

By Mike Fortunato, CIM®, FCSI®

image:FHM.com - Warner Bros.

In the first part of this article I introduced three types of risk: Volatility, Shortfall and Absolute. Today I’d like to continue from where we left off. There are literally dozens of other categories and subcategories of investment risk, but I’m going to restrict our discussion to just these three because many of the other risks I have not mentioned are actually related. Now that we’ve limited our discussion to just these three, I’d like to describe my observations regarding how many investors view and consider these risks, and I’ll offer an alternative point of view for consideration.

Volatility Risk

As I already mentioned, volatility risk is expressed by an investment’s standard deviation. It is a measure of how the price of an investment fluctuates over time. There are however, a few important aspects of this type of risk that I think are very important to mention:

- When we measure an asset’s standard deviation, we are measuring past fluctuations in price.

- An investment’s historical volatility can give us some insights into how it will behave in the future, but there is no guarantee that an investment’s future volatility will be the same as its historical volatility.

- Standard deviation measures absolute changes in price and treats rising prices and falling prices the same, but investors are usually more concerned about the negative consequences of falling prices verses the positive consequences of an investment rising in value.

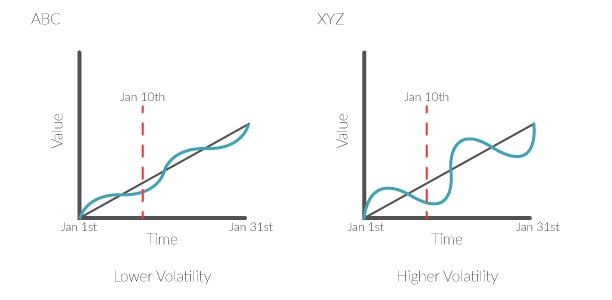

There is one aspect to volatility that I think is most important: when an investment’s market price falls in value it doesn’t necessarily mean you’ve lost any money, just like when an investment’s market price rises you haven’t necessarily gained any money. In order for an investor to realize an investment’s loss or a gain, they first need to sell their investment, and until they do sell we refer to their position as having a “paper-loss” or “paper-gain”. Volatility, as you recall, only measures the magnitude of an investment’s market price fluctuations. So simply holding a volatile investment has no real bearing on what your future loss or gain might be. In our illustration above, both ABC & XYZ ended at the same value: had both of them been sold on January 31st, the return for the investor would have been the same. Volatility, in this example, actually had no bearing on the rate of return. Volatility could have potentially affected the results if the investor had to sell either investment at some time between January 1st and January 31st. If for example, we had to sell on January 10th, XYZ would have experienced a greater loss than ABC.

In the scenarios I just described volatility only really matters in a situation when investors are compelled to sell their investment early during the chart. I’m not saying that all volatile investments eventually move towards a paper-gain, but what I am trying to highlight is that under certain conditions & assumptions other factors matter much more than volatility. Those other conditions & assumptions are:

- Your time horizon should complement your portfolio’s volatility.

- Your investments need to have a reasonable long-term rate of return.

- You are not compelled, for whatever reason, to prematurely sell your investments before your stated time horizon.

You might be thinking, why not just find an investment that has no volatility (basically just a straight diagonal line on the chart)? Those types of investments do exist; however, history has shown that there is somewhat of a trade-off between return and volatility. A GIC would be an example of an investment with basically zero volatility, but your real return (after-tax, inflation-adjusted) would be close to zero as well. Generally speaking, the market considers volatility when pricing assets, and assets that tend to be more volatility are typically valued in a manner that compensates investors for taking on the excess volatility risk. The end result is that, generally speaking, the assets that carry the most volatility also tend to carry the highest chance for long-term return. Investors who are cognizant of these facts can exploit them to their benefit by opting to hold the investments that provide a volatility discount while ensuring that their holding period insulates them from the potential negative effects of Volatility Risk.

Although understanding an investment’s potential volatility is important, I think some investors are paying too much attention to it for the wrong reasons. Many investors are conflating volatility with only losing money, and forgetting that the most volatile asset class: equities, tends to have the highest long-term returns. I can understand why investors are worried, as we all recall past high profile stocks that have gone bust, but that type of risk can be mitigated through proper diversification and fundamental due diligence. In my opinion, investors would be better served by trying to make their portfolio’s volatility complement their investment time horizon. Although it is logical to invest in the assets that will provide the best return over your time horizon, and ignore volatility that won’t affect their goal, many investors still find it challenging to watch the “paper-value” of their portfolios temporarily lose value. This often causes investors to alter the optimal composition of their portfolios in favour of an allocation that will provide less long-term return but with less overall volatility. Being overly conservative, however, is still better than the two other likely alternatives: overreacting and selling during a market drawdown, and, not investing at all.

I’ll end this instalment with one final note: Above, I presented a general concept about how I believe investors can maximize returns by ignoring volatility that doesn’t affect their long-term return. The tricky part is selecting investments that will provide that long-term return. I’m not suggesting that volatility causes investments to have high returns, but rather, I’m saying that often the investments with the best return might also have higher volatility. The goal of the investor should be finding the investments that will perform the best in their portfolio, regardless of the volatility of those investments: as long as they can tolerate the ups and downs without overreacting, and are not dependant on the portfolio for income or emergency cash.

In the next instalment I’ll take a closer look at Shortfall Risk, and hopefully illuminate some ways it can be managed.