Investing Is “Risky” Business – Shortfall Risk - Part 3 of 5

By Mike Fortunato, CIM®, FCSI®

image:FHM.com - Warner Bros.

In the first instalment of this article we introduced three types of risk: Volatility, Shortfall and Absolute. In the last instalment we took a closer a Volatility Risk. Today I’d like to examine Shortfall Risk and give you my perspective on how to best manage it.

Shortfall Risk

As you may recall, Shortfall Risk is the risk that an investment’s actual return will be less than the expected return needed to meet a financial obligation. Another way to think about shortfall risk is to say that it is the risk of falling short of an investment target or goal. To me, this is the most important risk because when it occurs it means you’ve failed to achieve your goal in your desired time frame. Oddly though, many investors don’t start seriously focusing on this risk until it is too late.

When it comes to shortfall risk I also think many investors are focusing too much on the variable that is the hardest to control: obtaining a high rate of return. Once a reasonable rate of return is achieved it becomes increasingly harder to put in more research and get more out in terms of added return. The law of diminishing returns seems to also apply to investment returns. Sure, with proper due diligence and adherence to sound portfolio management best practices it is possible to obtain a strong long-term rate of return, but far too many investors are banking on achieving double-digit returns to reach their long-term goals. I’m not saying that is impossible to achieve consistent double-digit returns, but it simply isn’t a realistic expectation for most investors.

Many investors would be better served if they focused less on rate of return and instead focused more on the other variables that they have more control over:

- The amount they contribute towards their goal.

- How frequently they contribute to their goal.

- How reasonable their goal is in relation to their time horizon.

Just to be clear, I’m not saying that striving for a high rate of return isn’t important, in fact, the previous instalment of this article talked about how I feel that under the right conditions, rate of return is more important than Volatility Risk; what I am trying to say is that investors need to understand what will impact their financial goal the most.

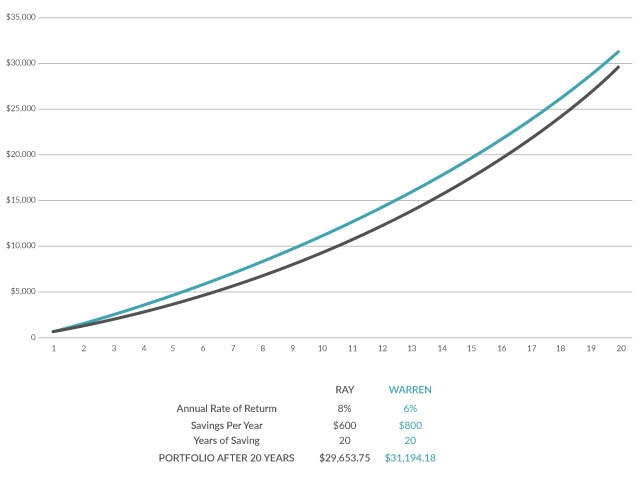

Here is an example to illustrate how important saving is in relation to rate of return. Let’s compare two different investors: Ray & Warren who both invest for a 20-year period. Ray earns a higher rate of return than Warren: 8% per year, but he saves less on an annual basis: only $600 per year. Warren, on the other hand, earns a lower rate of return at only 6% per year, but happens to saves more on an annual basis: $800 per year. Let’s see whose portfolio grows more after 20 years.

As you can see, even though Warren is earning a lower rate of return, he still comes out ahead because he was saving more each year. Also, we only used 6% as our forecast for Warren, which has a higher chance of materializing in real life instead of the 8% used for Ray. Certainly, it is possible to obtain a long-term return that is higher than 6%, but it is always helpful to be conservative in your estimates.

The other variable that investors have control over is how realistic their goal is in relation to their time horizon. I’m not going to suggest a specific formula to generate a realistic goal, because that would be an entire topic on its own, but I will highlight some general principles that are important to consider. The shorter your time horizon, the lower expected return you should use in your forecast. The reason for this is because you will want to limit your exposure to Volatility Risk if you don’t have the time to ride out the bumpy ups & downs of the market, and as I mentioned in the previous article, generally speaking, there are some trades-offs in return that come with less volatile investments. Yes, there are advanced portfolio building techniques you can employ to try to maximize your growth while keeping your volatility in check, but as we saw in the above example a few extra percent of growth each year is less important than trying to find ways to save more towards your end goal – especially with shorter time horizons. Also, extra return will help a lot over longer time horizons, but as we learned in the previous instalment of this article, exposure to volatility risk becomes less important when your time horizon is shorter.

In summary, Shortfall risk is one of the most important risks investors face because it is literally the risk of failing to achieve their goal. The best way to minimize Shortfall is to first ensure your goal is realistic in terms of the rate of return you need to assume to reach the goal within your time horizon. Then do everything you can to maximize how much you save and contribute to your goal over time. These are the variables you have the most control over. In the next instalment of this article we’ll examine the third and last type of risk: Absolute Risk.