Beware of the Writing on The Wall – Part 1 - The Bull Market Leading Up To The Crash

By Mike Fortunato, CIM®, FCSI®

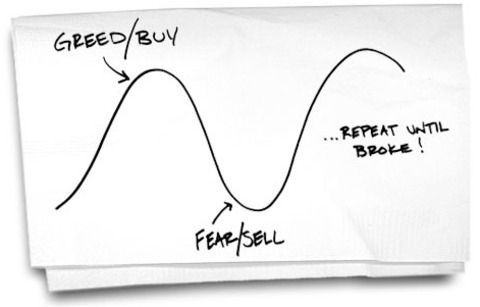

image: http://metuchenliving.com/why-do-we-sell-low-and-buy-high/

Eleven years ago, in the summer of 2007, I landed my first finance related job as a bank teller for one of Canada’s Big Five national banks. Like most entry level roles, being a bank teller taught me valuable lessons about customer service, organization, problem solving, and teamwork. It also gave me a great introductory view of the broader finance industry that I still work in today. When I started my career at the bank, my goal was to eventually work with investments. Now that I’m a member of a portfolio management team I still find myself leveraging knowledge about economics, markets and investments that I picked up while I was a teller over 10 year ago. The most important lessons I learned however, didn’t come from the training or mentorship I received, but instead came from simply observing our clients’ reactions to the global financial system that was collapsing around us all during a period that we now call: The Great Recession (or 2008 Financial Crisis).

Just a few months after processing my first bank deposit I watched the world’s equity markets fall into complete pandemonium. During the year and a half that followed, the world experienced a terrifying bear-market where stock prices plummeted from all-time highs to levels not seen for almost a decade. Being a teller during that time was like having a front row seat to watch the panic unfold. On a daily basis I observed my branch’s customers and advisors trying to make sense of chaos. I remember thinking to myself at the time, “how is it that so many people didn’t see this coming?”. In the weeks leading up to the crash I recall that many analysts on the financial news, and most of the investors I spoke with, were actually quite bullish. Their positive outlook even continued into the first few months of the crash, when each new market low was often celebrated as an opportunity to double-down in anticipation of a correction bottom that never seemed to arrive. While trying to make sense of all that was unfolding I noticed a phenomenon that gave me tremendous insight into the interplay between market fundamentals and basic investor psychology: the most expensive and riskiest investments are often the most attractive to investors who don't understand the cyclical nature of markets.

As a bank teller I was stationed at the font of the branch directly facing a wall of promotional posters that the bank had setup to drive various product offerings. A large part of my role involved answering client’s questions about those posters. The bank’s marketing team would periodically change the content advertised on the posters to coincide with whatever new campaign the bank was promoting at that time. Every time the posters changed, the bank’s clients would come to me to inquire about the writing on the wall. Being on the front lines literally put me in the best position to observe both the timing of the bank’s investment offerings and the client’s reaction to them. Overlaying both these observations against the backdrop of The Financial Crisis as it was unfolding, was a revelation into the powerful micro-economic forces that drive market cycles. Since acquiring this knowledge 10 years ago, I’ve witnessed this powerful phenomenon play out several other times in many other markets: the stock market, forex, commodities and multi-unit residential real estate market. The next three instalments of this article will focus specifically on the how this dynamic unfolded: during the bull-market leading up to the crash, during the crash itself and finally, during the recovery that followed.